Details Released of the Canada Emergency Wage Subsidy Extension to December 19, 2020 and Other Updates

Canada Emergency Wage Subsidy

The federal government has extended the Canada Emergency Wage Subsidy (CEWS) until December 19, 2020.

Enhanced Eligibility

The government has made the subsidy accessible to a broader range of employers by eliminating the requirement for a minimum 30 percent revenue decline.

Effective retroactively to July 5, 2020, the CEWS will consist of two parts:

- A base subsidy available to all eligible employers who are experiencing a decline in revenues, with the subsidy amount varying depending on the scale of revenue decline; and

- A top-up subsidy of up to an additional 25 percent for those employers who have been most adversely affected by the COVID-19 crisis.

Base Subsidy

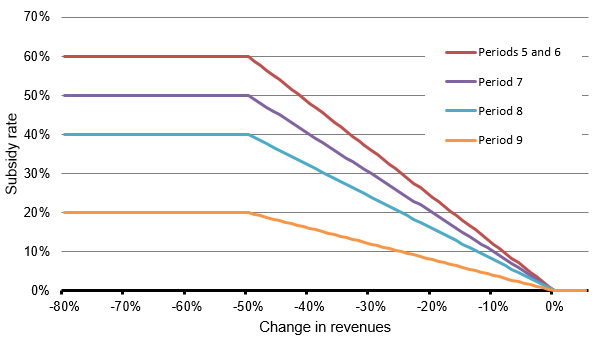

The base CEWS would be a specified rate, applied to the amount of remuneration paid to the employee for the eligibility period, on remuneration of up to $1,129 per week as shown in the table below

| Timing | Period 5*: July 5 – August 1 | Period 6*: August 2 – August 29 | Period 7*: August 30 – September 26 | Period 8: September 27 – October 24 | Period 9: October 25 – November 21 |

| Maximum weekly benefit per employee | Up to $677

| Up to $677

| Up to $565

| Up to $452

| Up to $226

|

| Revenue drop: | | ||||

| >50% | 60% | 60% | 50% | 40% | 20% |

| 0% – 49% | 1.2 x revenue drop (e.g., 1.2 x 20% revenue drop = 24% base CEWS rate) | 1.2 x revenue drop (e.g., 1.2 x 20% revenue drop = 24% base CEWS rate) | 1.0 x revenue drop (e.g., 1.0 x 20% revenue drop = 20% base CEWS rate) | 0.8 x revenue drop (e.g., 0.8 x 20% revenue drop = 16% base CEWS rate) | 0.4 x revenue drop (e.g., 0.4 x 20% revenue drop = 8% base CEWS rate) |

* In Periods 5 and 6, employers who would have been better off in the CEWS design in Periods 1 to 4 would be eligible for a 75-percent wage subsidy if they have a revenue decline of 30 percent or more (see safe harbour rule below).

Chart of subsidy amounts at various revenue drops:

Top-up Subsidy

A top-up subsidy of up to 25 percent will be available to employers who were the most adversely impacted by COVID-19. The top-up will be determined based on the revenue drop experienced by an eligible employer when comparing revenues in the preceding three months to the same months in the prior year. The alternative approach to the calculation of baseline revenues remains.

The following chart illustrates the calculation of the top-up:

| 3-month average revenue drop | Top-up CEWS rate | Top-up calculation = 1.25 x (3-month revenue drop - 50%) |

| 70% and over | 25% | 1.25 x (70%-50%) = 25% |

| 65% | 18.75% | 1.25 x (65%-50%) = 18.75% |

| 60% | 12.5% | 1.25 x (60%-50%) = 12.5% |

| 55% | 6.25% | 1.25 x (55%-50%) = 6.25% |

| 50% and under | 0.0% | 1.25 x (50%-50%) = 0.0% |

Safe harbour rule for Periods 5 and 6

For Periods 5 and 6, an eligible employer would be entitled to a CEWS rate not lower than the rate that they would be entitled to if their entitlement were calculated under the CEWS rules that were in place for Periods 1 to 4. This means that in Periods 5 and 6, an eligible employer with a revenue decline of 30 per cent or more in the relevant reference period would receive a CEWS rate of at least 75 per cent or potentially an even higher CEWS rate using the new rules outlined above for the most adversely affected employers (up to 85 per cent).CEWS for Furloughed Employees

For Periods 5 and 6, the subsidy calculation for a furloughed employee will remain the same as for Periods 1 to 4.

Beginning in Period 7, CEWS support for furloughed employees will be adjusted to align with the benefits provided through the Canada Emergency Response Benefit (CERB) and / or Employment Insurance (EI). This will ensure equitable treatment of employees on furlough between both programs.

For Period 5 and subsequent periods, the CEWS for furloughed employees will be available to eligible employers who qualify for either the base rate or the top-up for active employees in the relevant period.

The employer portion of contributions in respect of the Canada Pension Plan, Employment Insurance, the Quebec Pension Plan, and the Quebec Parental Insurance Plan in respect of furloughed employees will continue to be refunded to the employer.

Calculating Revenues

An employer's revenue for the purposes of the CEWS is its revenue in Canada earned from arm's-length sources. Revenues from extraordinary items and amounts on account of capital are excluded.For registered charities and non-profit organizations, the calculation includes most forms of revenue, excluding revenues from non-arm's length persons. These organizations are allowed to choose whether to include revenue from government sources as part of the calculation. Once chosen, the same approach would have to apply throughout the program period.

Special rules for the computation of revenue are provided to take into account certain non-arm's-length transactions, such as where an employer sells all of its output to a related company that in turn earns arm's-length revenue. As well, affiliated groups are able to elect to compute revenue on a consolidated basis.